Which savings account is right for your employees?

When it comes to saving, Canadians are increasingly favouring Tax-Free Savings Accounts (TFSAs) over Registered Retirement Savings Plans (RRSPs), according to data from Statistics Canada.

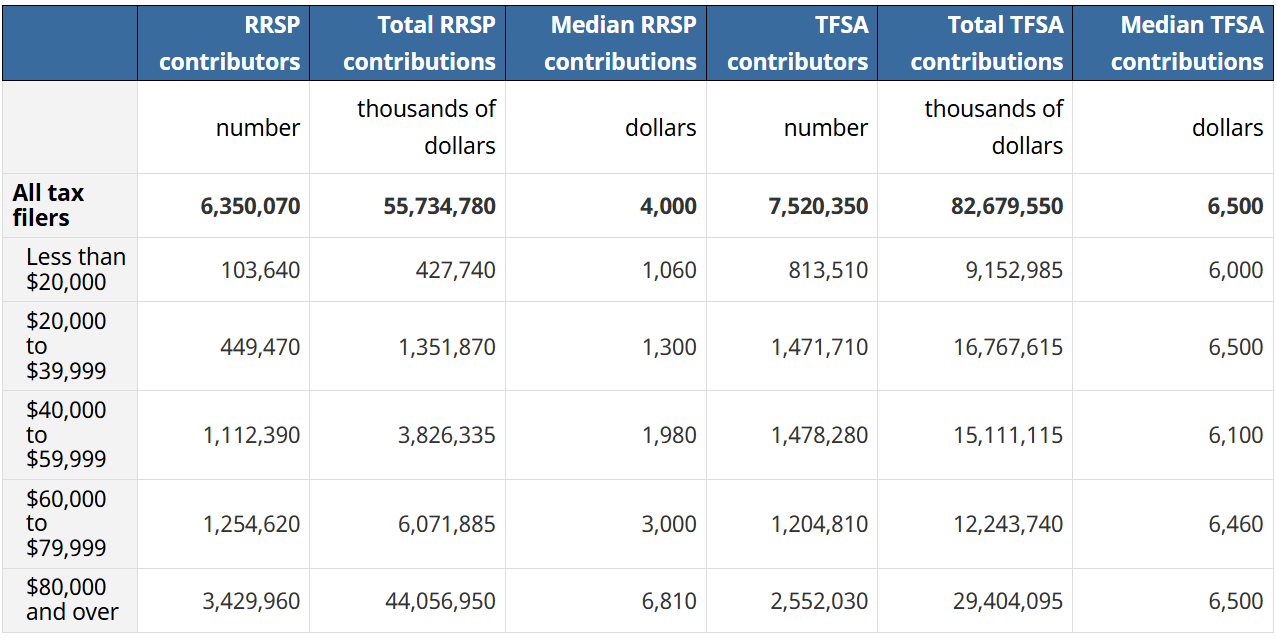

In 2023, 11.3 million tax filers contributed to either an RRSP or a TFSA.

Of those, 3.8 million contributed only to an RRSP, with a median contribution of $3,420. Another five million tax filers contributed only to a TFSA, with a median contribution of $6,500—the maximum allowable contribution for 2023.

A smaller group—2.5 million tax filers—contributed to both, with median contributions of $5,000 for RRSPs and $6,150 for TFSAs.

“Among working age groups (25 to 64 years), median RRSP and median TFSA contributions evolved in a similar manner, increasing with each age group. This similarity between medians did not appear when grouped by income,” said StatCan.

“Median TFSA contributions in all income groups varied little (ranging from $6,000 to $6,500), while median RRSP contributions varied from $1,060 for contributors with income of less than $20,000 to $6,810 for those with income of $80,000 or more.”

Canadians’ TFSA values hit record highs of just under $45,000 in 2024, an increase of 8% over the previous year, according to the BMO Financial Group.

What is the difference between an RRSP and TFSA?

An RRSP is designed primarily for retirement savings. Its key features include:

Tax-deductible contributions: Contributions can be deducted from your taxable income, potentially reducing the amount of income tax you owe.

Tax-deferred growth: Investment income earned within the RRSP is not taxed as long as it remains in the plan. Taxes are deferred until funds are withdrawn, typically during retirement when you may be in a lower tax bracket.

Contribution limits: The annual contribution limit is based on 18% of your previous year's earned income, up to a maximum amount set by the government each year.

Withdrawals: Withdrawals are fully taxable as income. Early withdrawals may be subject to withholding taxes and can impact government benefits.

Meanwhile, a TFSA offers flexible savings for various purposes. Key features include:

After-tax contributions: Contributions are made with after-tax income and are not deductible from your taxable income.

Tax-free growth and withdrawals: Investment income and withdrawals are tax-free, providing flexibility for both short-term and long-term savings goals.

Contribution limits: The government sets annual contribution limits. Unused contribution room accumulates and can be carried forward indefinitely.

Withdrawals: Withdrawals can be made at any time without tax consequences and do not affect eligibility for government benefits. Withdrawn amounts are added back to your contribution room in the following year.

Each account has its advantages. RRSPs offer immediate tax relief by reducing taxable income and encouraging long-term savings. However, withdrawals are taxed as income and may affect government benefits such as Old Age Security (OAS) and the Guaranteed Income Supplement (GIS).

TFSAs, on the other hand, offer unmatched flexibility. There are no penalties for withdrawals, and funds can be used for any purpose. Withdrawals do not impact eligibility for government benefits. That said, TFSA annual contribution limits are lower than RRSP limits, which may restrict tax-free saving potential.

For 2025, the TFSA contribution limit is $7,000, compared to $32,490 for RRSPs.

Helping employees maximize RRSP, TFSA savings

To help employees maximize the benefits of these savings vehicles, the government of Canada advises employers to follow this four-step process when contributing:

- Determine if the benefit is taxable

- Calculate the value of the benefit

- Withhold payroll deductions and remit GST/HST

- Report the benefit on a slip

Long-term employment does not guarantee comfortable retirement for many workers, based on findings from a recent study. That’s because financial stress is still the top worry for workers aged 40 to 60, according to Healthcare of Ontario Pension Plan (HOOPP).