How much do Canadians need to retire?

Amid Canadians’ worries about saving for their post-work life, contributions to registered retirement savings plans (RRSPs) are on track to hit a record high this year.

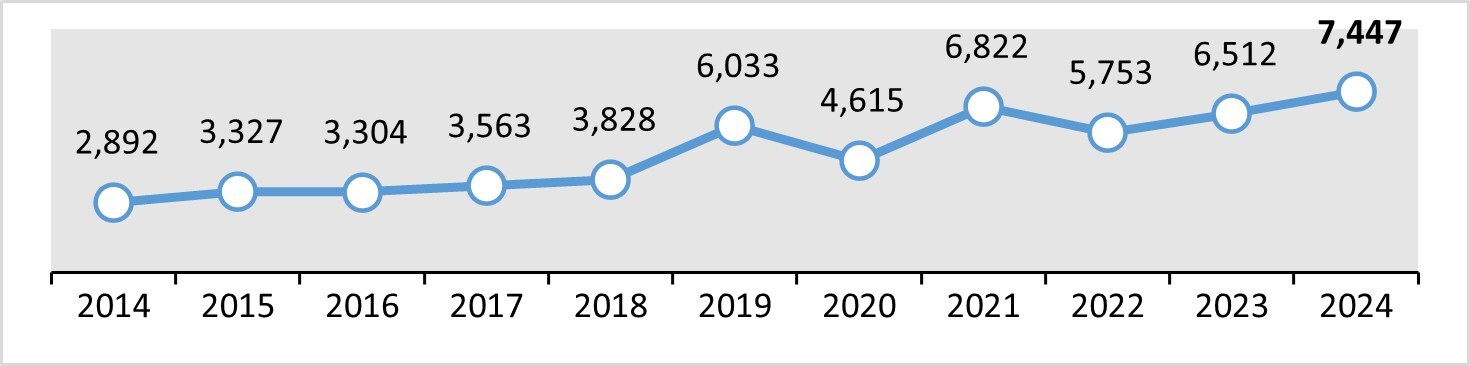

For 2025, annual RRSP savings are projected to reach $7,447, a 14% increase over last year ($6,512), reports BMO Financial Group.

The recent number is also $625 more than the current record-high $6,822, according to the report.

"Many Canadians continue to show resilience, making saving and investing in their retirement a top priority," says Brent Joyce, chief investment strategist and managing director, BMO Private Investment Counsel.

"For Canadian investors, one of the best ways to make financial progress and stop rising prices from eroding retirement savings over the long term is to have a portfolio designed to mitigate inflationary pressures, while also taking other factors like investment time horizon and risk tolerance into account. Investors may also want to consider speaking with an investment advisor when looking for ways to help reduce the impact of inflation on their portfolio."

Canadians’ Tax-Free Savings Account (TFSA) values hit record highs of just under $45,000 in 2024, an increase of 8% over the previous year, BMO Financial Group previously reported.

Currently, over three-quarters of Canadians (76%) are worried they will not have enough money in retirement because of rising prices, according to BMO’s survey of 1,500 adult Canadians conducted in November 2024.

And 63% of Canadians believe rising prices over the past 12 months have limited their ability to save for retirement. Among this group, the top four ways they are adjusting their financial planning are:

Cutting other spending to maintain current retirement savings levels

Putting less into retirement savings

Planning on working longer

Putting off retirement savings completely

"Inflation is a major concern for Canadians, and the spike in prices as the economy emerged from the pandemic is a stark reminder rising prices can affect spending, investment and savings plans," said Robert Kavcic, Senior Economist, BMO. "Inflation should always be a major consideration when saving and investing for retirement and if investors have concerns about how rising prices may impact their retirement savings, it may help to seek guidance from a financial professional."

Overall, Canadians surveyed believe they will need just over $1.54 million to retire, down from $1.67 million in 2023.

Nearly half (46%) of non-retired Canadians prioritize spending on their current lifestyle in place of saving for retirement, mainly due to paying off debts (38%) or preferring to enjoy their life now (18%), according to a previous IG Wealth Management report.

Low participation rates in retirement savings options and high debt loads are two of the biggest reasons workers struggle to save for retirement, according to Chris Magno, senior vice president and general manager, ADP Retirement Services.

Employers can help workers prepare for life after work by doing the following, he says:

Promote financial literacy.

Offer workers catch-up contributions for retirement savings.

Simplify retirement plan administration.

“A thoughtfully designed retirement plan with varied options, education and automation instills loyalty, trust and a sense of partnership,” Magno says. “Employees who feel backed in their long-term goals are more engaged and invested in the organization’s success.”

Target retirement readiness education can also be crucial to help employees, according to Gallagher.

“Employers can better equip their employees for the future through access to targeted education and vetted financial advisors. Not only does one-on-one consultation support appropriate retirement income, but it also helps define the path forward for spending accumulated funds while accounting for healthcare costs and lifestyle, among other factors.

“Retirement readiness workshops, educational resources and communications establish financial literacy and address issues for employees.”

If employers provide workers with 100% matching contributions for their retirement savings, they can help workers retire a couple of years early, according to a previous Mercer Canada report.