Savings goal for retirement increases by nearly 30% to $900,000

Most Canadians are afraid they may not have enough cash saved up for life after work. In fact, 61% of Canadians fear running out of money in retirement, reports CPP Investments.

This anxiety is even more pronounced among adults aged 28 to 44 (67%), and is felt more strongly by women (66%) than men (55%).

Adding to the stress is the fact that over the past year, Canadians have raised their retirement savings goal from $700,000 to $900,000 – a nearly 30% increase in just 12 months.

“Based on our survey, running out of money in retirement is a real worry for Canadians, which is understandable given life expectancy is on the rise,” said Michel Leduc, senior managing director & global head of Public Affairs and Communications, CPP Investments. “This underscores the importance of building a solid understanding of your personal finances and seeking resources to improve financial literacy to help you manage money more effectively.”

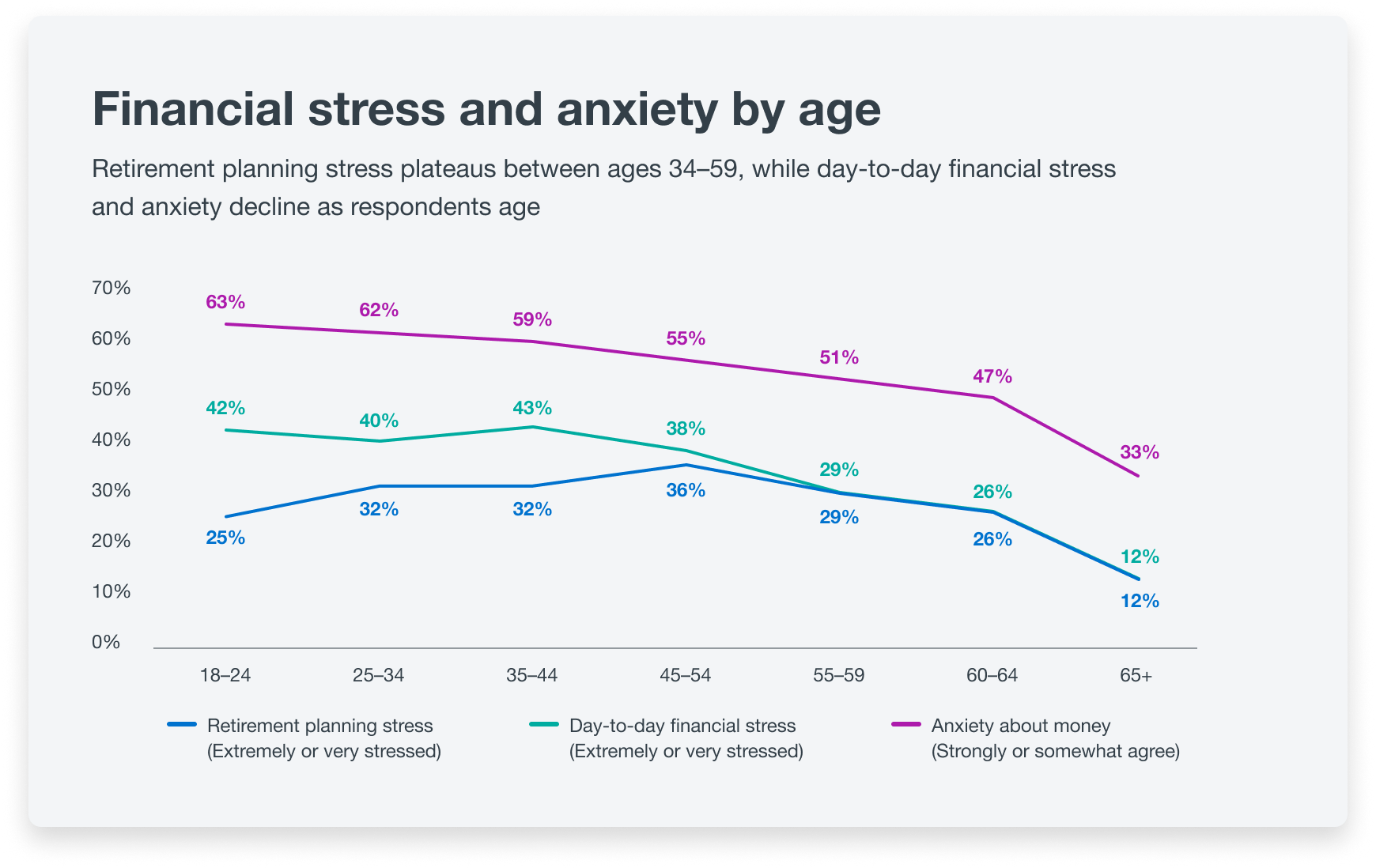

Currently, nearly six in 10 Canadians report feeling financial stress daily. On a positive note, financial stress decreases as workers age, according to CPP Investments’ survey of nearly 4,800 workers, conducted by Innovative Research Group from Aug.1 to 7, 2024.

Source: CPP Investments

Currently, over two in five (41%) of Canadians belong to the financially stressed cluster, according to a previous report from the National Payroll Institute. That number is up from 37% in 2023.

One good thing working for Canadian workers is that, overall, more than 22 million Canadians have a base for their retirement plan through the Canada Pension Plan (CPP), according to CPP Investments.

“Working Canadians are already saving for their retirement through their CPP contributions,” Leduc said. “One thing that Canadians have that protects them is that their CPP benefits are payable as long as they live and are indexed to inflation.”

Recognizing the value of the CPP can boost confidence in having enough money for retirement, notes CPP Investments. That’s because only 24% of Canadians aged 35 to 64 who are unfamiliar with the CPP believe their savings will last throughout their retirement. In contrast, 71% of those very familiar with the CPP feel confident about their savings.

“Knowing you already have a head start through the CPP can help make retirement feel more achievable and can hopefully alleviate some of the stress people have about saving for retirement,” Leduc said.

Overall, 51% of Canadians believe their retirement savings are falling behind, according to a previous report from Manulife.

Here are four ways to help your employees save for retirement, according to J.P. Morgan:

Nearly six in 10 (58%) Canadian households have reduced day-to-day expenses in response to financial strain over the last year, according to a previous report from the World Financial Group (WFG).