Layoffs and fewer quits show rate rises are starting to slow the economy

The U.S. labor market showed some softening in March as job openings fell for the third consecutive month and layoffs increased to their highest level in over two years.

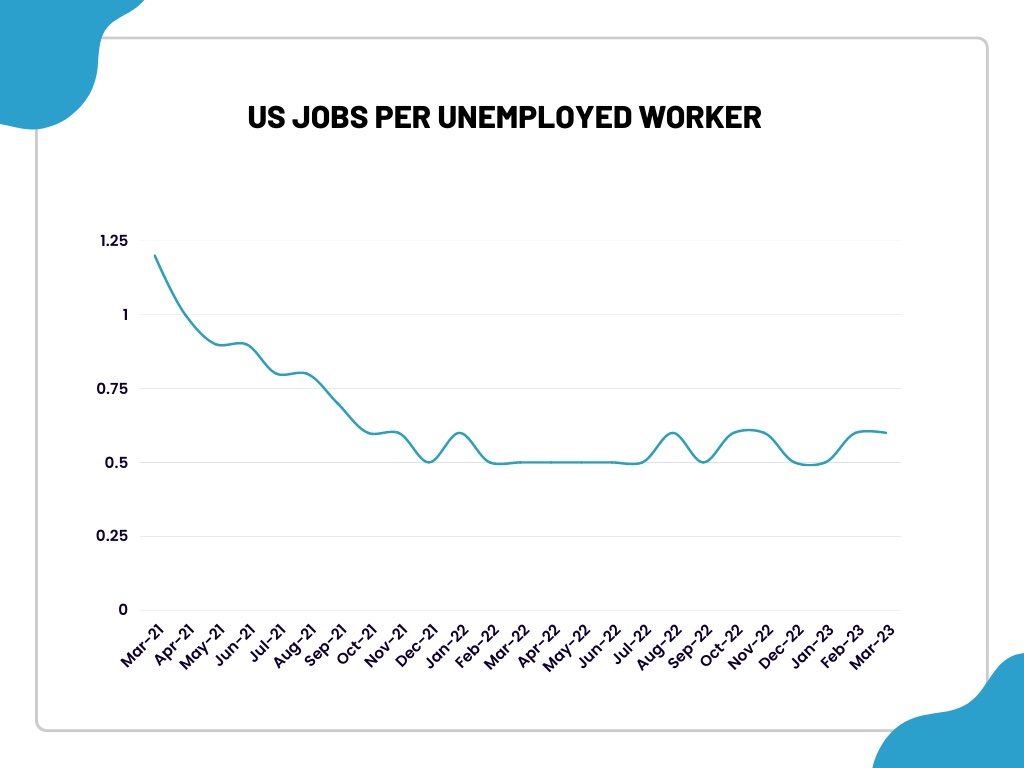

The monthly Job Openings and Labor Turnover Survey (JOLTS) report from the Labor Department indicated that there were 1.6 vacancies for every unemployed person in March, the lowest reading since October 2021.

Despite this news for employers, the labor market remains tight with the ratio still above the 1.0-1.2 range that economists say is consistent with a jobs market that is not generating too much inflation.

Federal Reserve officials are closely monitoring this ratio, which will be welcomed by the Fed as it indicates a reduction in excess demand for labor. However, with the ratio still higher than at any time prior to November 2021, the labor market remains tight by historical standards.

"The job openings and quits rates remain historically high, and the layoff rate remains historically low, but all three are moving in the direction of a cooler labor market," Michael Feroli, chief U.S. economist at JPMorgan in New York told Reuters.

"The signs of labor market softness won't be a game-changer for tomorrow's Fed meeting, though they do suggest that the cumulative amount of policy tightening is starting to have its desired effect on businesses' labor demand."

The decline in job openings in March was particularly evident in small businesses, with one to 49 employees, which have been the main drivers of the labor market's phenomenal growth. There were also significant declines in job openings in transportation, warehousing, and utilities, professional and business services, and retail.

The JOLTS report shows that hiring has remained steady at 6.1 million, maintaining the hiring rate at 4.0%. However, economists anticipate that April's employment report, set to be released on Friday, will reveal a slowdown in labor demand.

The JOLTS report also indicated a significant increase in layoffs, rising by 248,000 to 1.8 million, the highest level since December 2020. The construction industry saw the largest loss of positions at 112,000, likely reflecting the impact of job losses in the housing market due to higher mortgage rates.

Additionally, accommodation and food services lost 63,000 jobs, while the health care and social assistance sector reported 42,000 layoffs, with employment in the leisure and hospitality sector still below pre-pandemic levels.

Small and medium-sized businesses accounted for most of the layoffs in the professional and business services category, with all four regions reporting increases in job losses. The layoffs and discharge rate increased to 1.2%, the highest since December 2020, from 1.0% in February.

The decline in job openings and the rise in layoffs have resulted in fewer voluntary resignations. Resignations have dropped to 3.85 million, the lowest level since May 2021, from 3.98 million in February, with declines in the accommodation and food services sector, and drops in the South and West regions, but increases in the Northeast and Midwest regions.

The quits rate, which is seen as a measure of labor market confidence, has dipped to 2.5% from 2.6% in February, down from the 2.9%-3.0% range seen in late 2021 and early 2022 when job hopping was at its peak.

The U.S. central bank is expected to raise its benchmark overnight interest rate by another 25 basis points to the 5.00%-5.25% range today, in what is the fastest monetary policy tightening campaign since the 1980s. The decline in job openings is expected to aid the Fed in its fight against inflation.

Investors on Wall Street were trading lower, focusing on a warning by Treasury Secretary Janet Yellen that the federal government could run out of money within a month amid a standoff to raise its $31.4 trillion borrowing cap. The dollar also fell against a basket of currencies, while U.S. Treasury prices rose.